Alternative Data is Changing Credit.

What is Alternative Data and how do you get started?

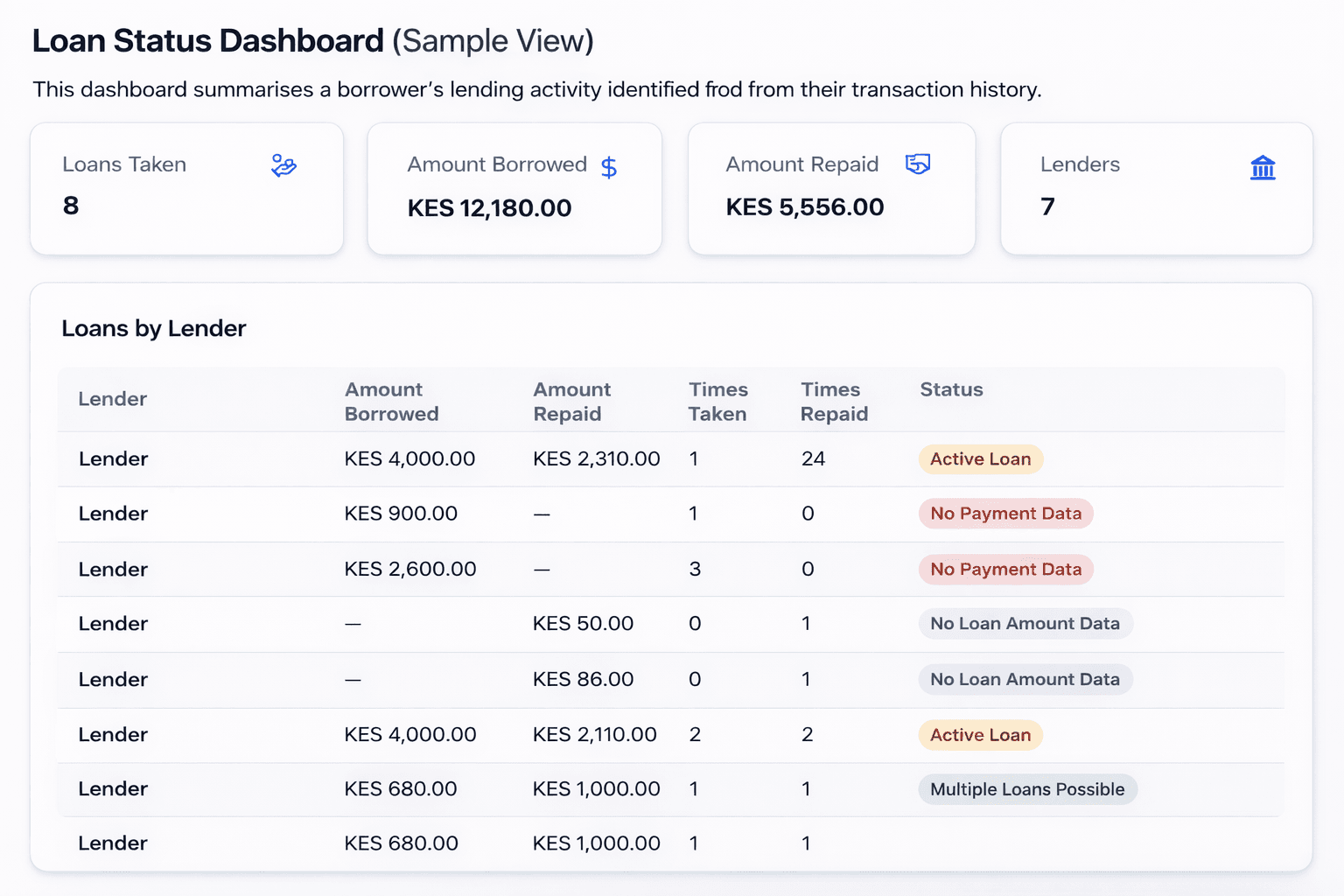

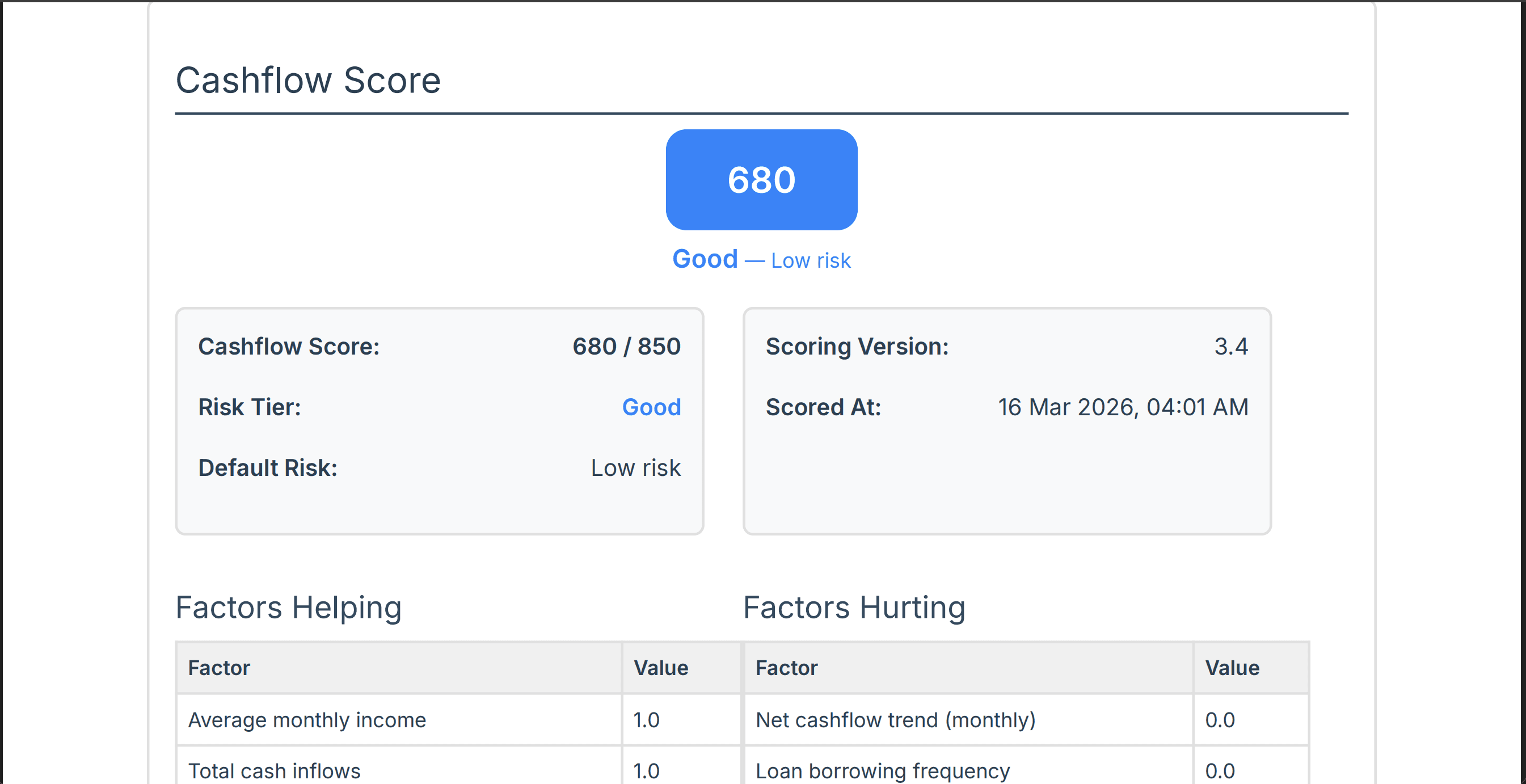

As credit underwriting turns from common sense and logic-driven to - Machine learning, AI, and Big Data Analytics; Lenders are moving from relying solely on traditional reports to checking account transactional data such as online shopping habits, savings patterns, and even utility payments to paint a far richer picture of borrowers.

Where is the change?

This new data source, i.e. Alternative Data, is proving to be the most significant input that will differentiate the next few years from what we have seen in the past.

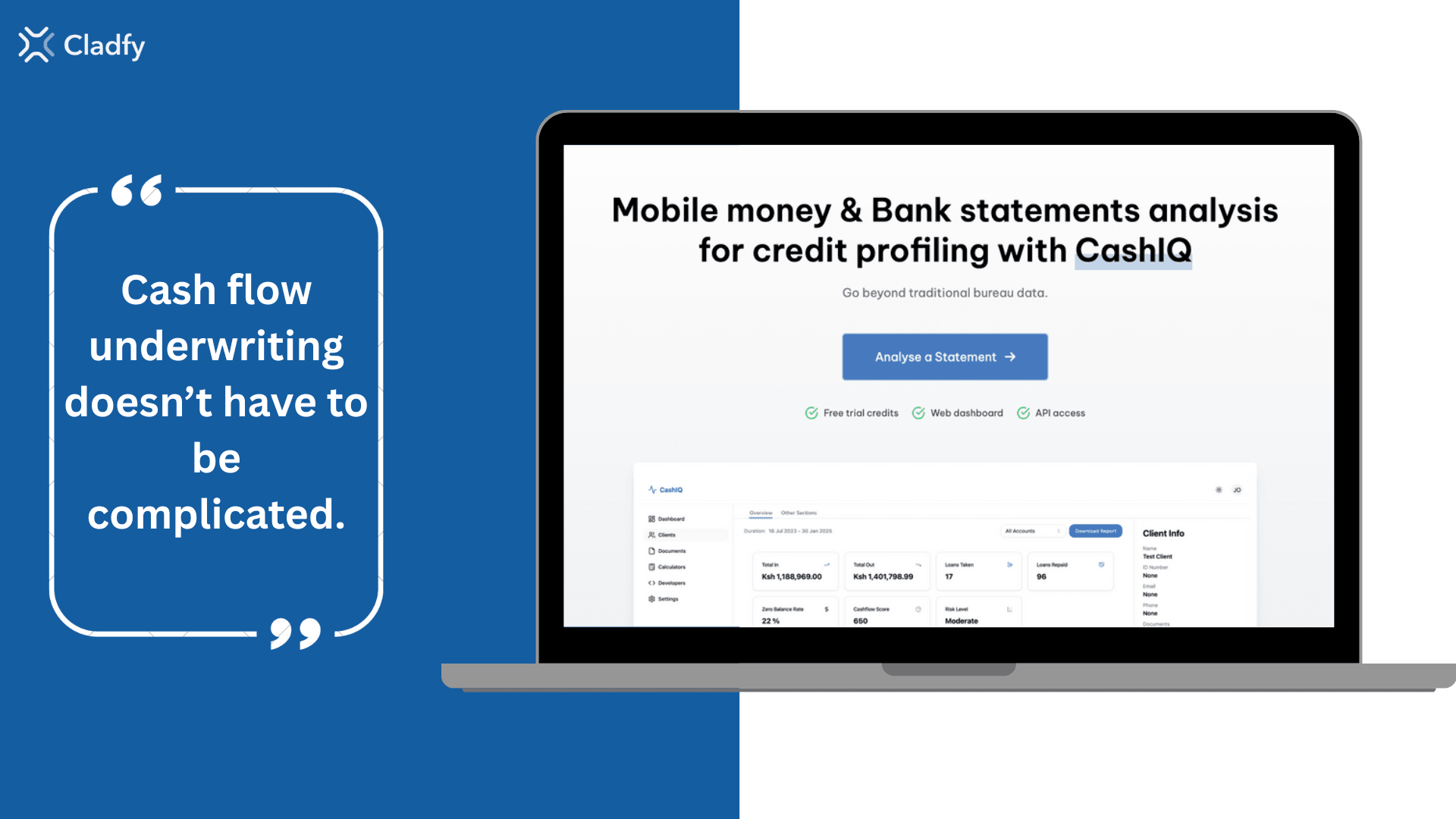

By leveraging consumer permission to access one of the richest data sources of underwriting, the checking/transactions account data, lenders can control more variables as they serve new segments of borrowers.

What should a lender do?

Invest in technology and expertise.

Create flexible underwriting models.

Embrace transparency and ethical practices

By anticipating this change and partnering with an established player, credit issuers can speed up the transition to implementing Cash-flow data Analysis in their underwriting processes.

Conclusion

By embracing this revolution, lenders can unlock expanded reach, accurate decisions, better portfolios, and most importantly, the trust of borrowers and regulators in this exciting new era of credit.

Let us help you get ahead of the curve using our software solutions for cash-flow data analysis;

Email us at info@cladfy.com

See our API Docs at https://cladfy.readme.io/