Cladfy — Loan Status & Cashflow Scoring Guide

A lender's guide to interpreting loan statuses and cashflow scores in Cladfy reports.

Search for a command to run...

A lender's guide to interpreting loan statuses and cashflow scores in Cladfy reports.

No comments yet. Be the first to comment.

This blog series explores how Cladfy is leveraging innovative technology to unlock the potential of cash flow data, enabling more inclusive and accurate credit assessment and lending decisions.

A lender's guide to an AI-powered default prediction score.

A lender's guide to an AI-powered default prediction score.

Using an Annualized Interest Rate - a 25% for 6 Weeks example If you’re a lender offering short-term loans, you’ve probably dealt with Flat Interest Loans that run for just a few weeks.Let’s say you want to create a loan product that charges a 25% fl...

No black-boxes, no unnecessary complexity—just clear, data-backed decision-making.

Simple, intuitive signals can drive smarter credit decisions

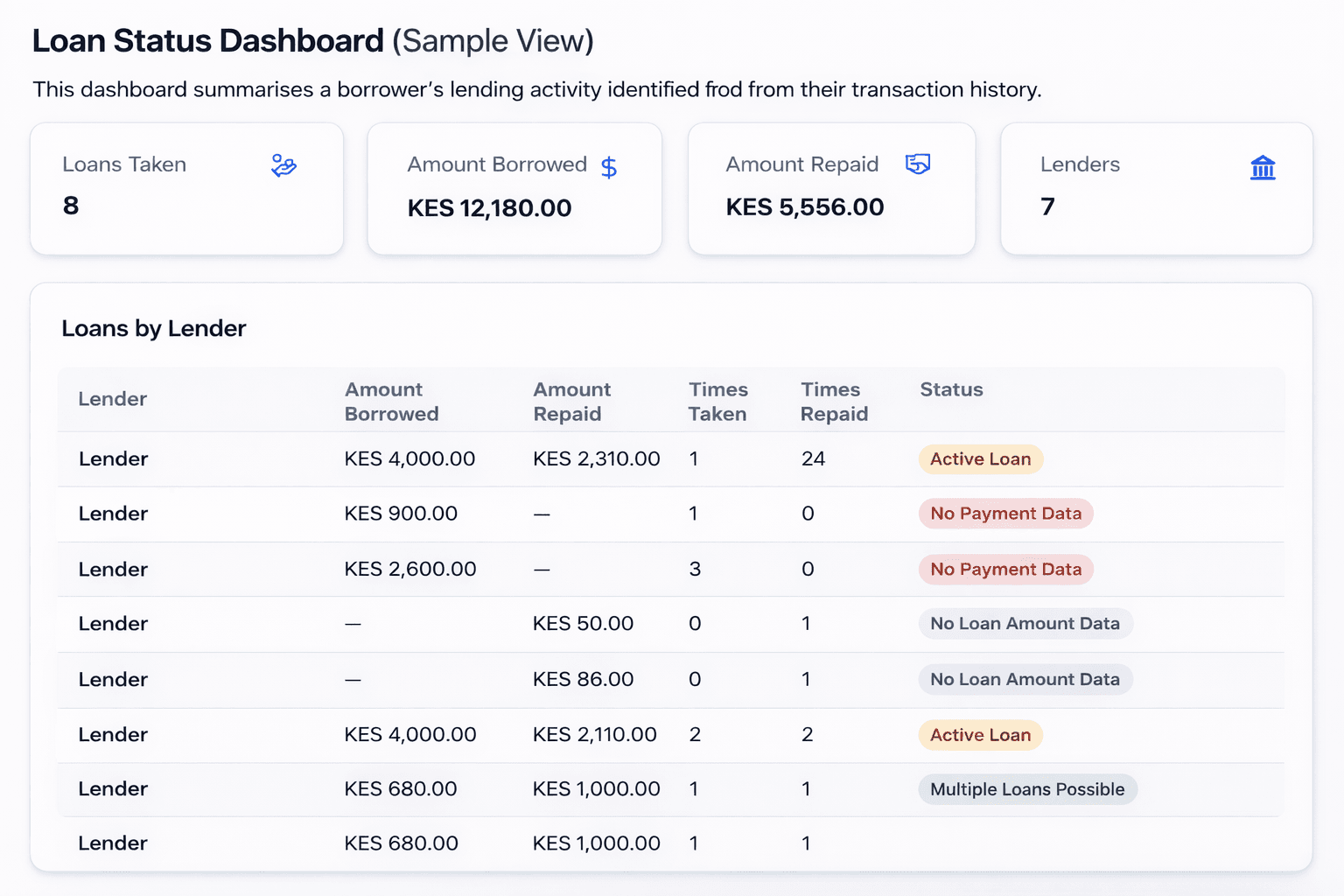

Each lender relationship is assigned a loan status based on transaction analysis.

| Status | Meaning |

|---|---|

| 🟢 Fully Paid | Loan appears fully repaid. No outstanding obligation. |

| 🟢 Multiple Loans Possible | The loan appears over-repaid. This may occur due to interest, fees, charges, or an additional loan taken after the first was repaid. No confirmed outstanding obligation. |

| 🔵 Likely Settled | Most of the loan was repaid, and there has been no recent activity. The loan was likely discounted, written off, or settled. |

| 🟡 Active Loan | There is recent activity and an outstanding balance. This represents a current credit obligation. |

| ⚪ Limited Data | Loan activity exists, but repayment or disbursement information is incomplete. |

Active Loan → Treat as current debt.

Likely Settled / Fully Paid / Multiple Loans Possible → Do not treat as active credit unless further evidence suggests otherwise.

Limited Data → Ask the borrower for clarification.

Important: If the report only shows repayments but no loan disbursement, the client may be repaying a loan on behalf of someone else, or the loan may have been taken outside the statement period. In such cases, request additional information from the borrower.

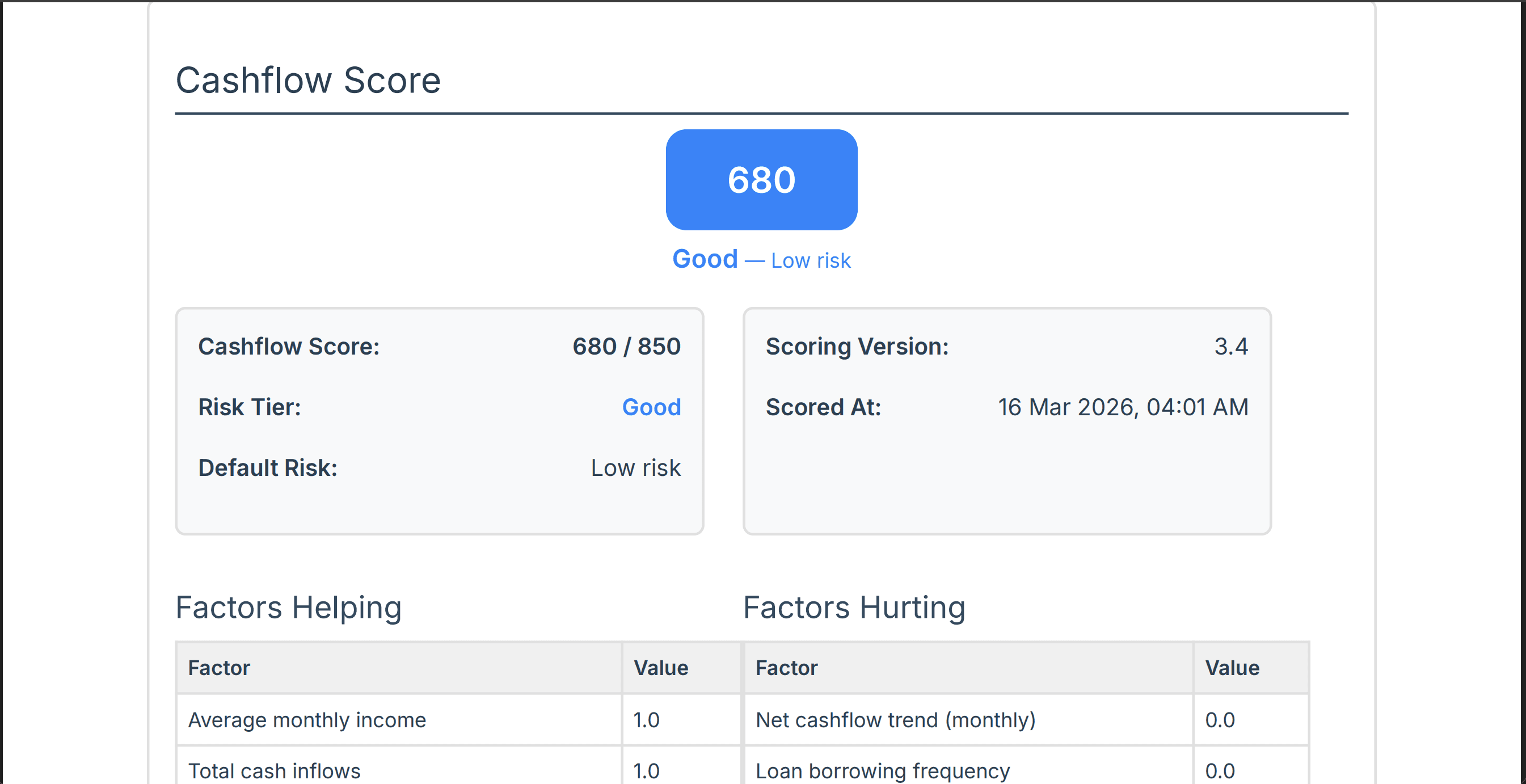

The Cashflow Score estimates a borrower's credit risk using transaction behaviour from bank or mobile money statements.

The score reflects patterns such as:

Income stability

Spending behaviour

Credit usage

Cashflow consistency

Financial discipline signals

The score does not rely on credit bureau data and is calculated solely from the statement provided.

| Score Range | Risk Level |

|---|---|

| 780–850 | Very Low Risk |

| 680–779 | Low Risk |

| 560–679 | Moderate Risk |

| 400–559 | High Risk |

| 300–399 | Very High Risk |

Higher scores indicate stronger financial behaviour and lower default risk.

Recommended review flow:

Check the risk tier for overall borrower risk.

Review Active Loans to understand current obligations.

Ignore Fully Paid, Likely Settled, or Multiple Loans Possible statuses when calculating debt burden.

Review highlighted factors to understand key strengths or risks in the borrower profile.

The score should support credit decisions, not replace lender judgment.

The score reflects only the uploaded statement period.

Results may change when new transactions are analysed.

If income or repayments occur in another account not included in the statement, they may not appear in the analysis.