What is a Repayment-Score and how does it affect credit decisions

A practical guide for lenders!

Search for a command to run...

A practical guide for lenders!

No comments yet. Be the first to comment.

Lenders need to track a variety of metrics to ensure the success of their business. However, five process-based metrics are particularly important: By tracking these metrics, lenders can gain insights into their lending operations and make infor...

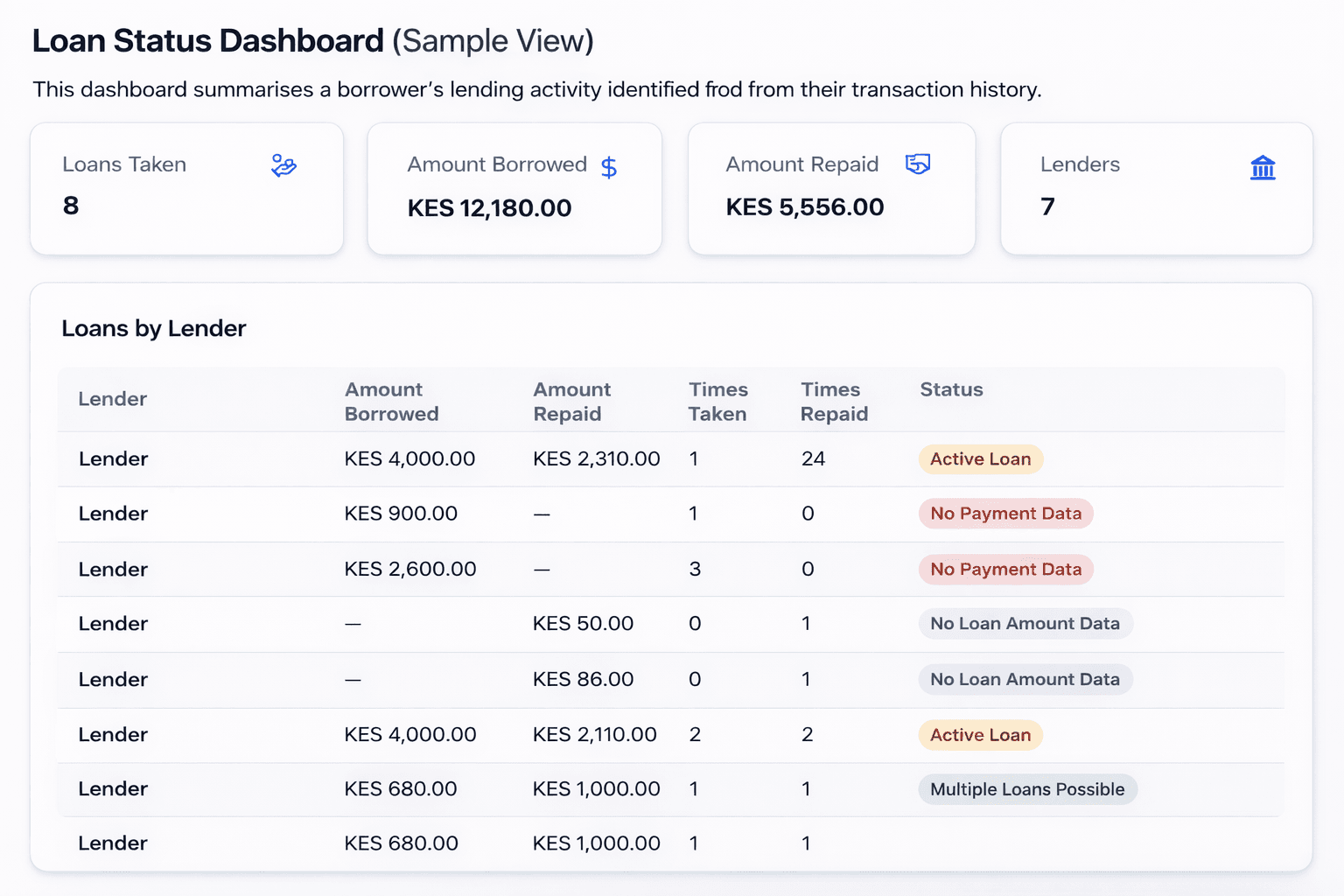

A lender's guide to interpreting loan statuses and cashflow scores in Cladfy reports.

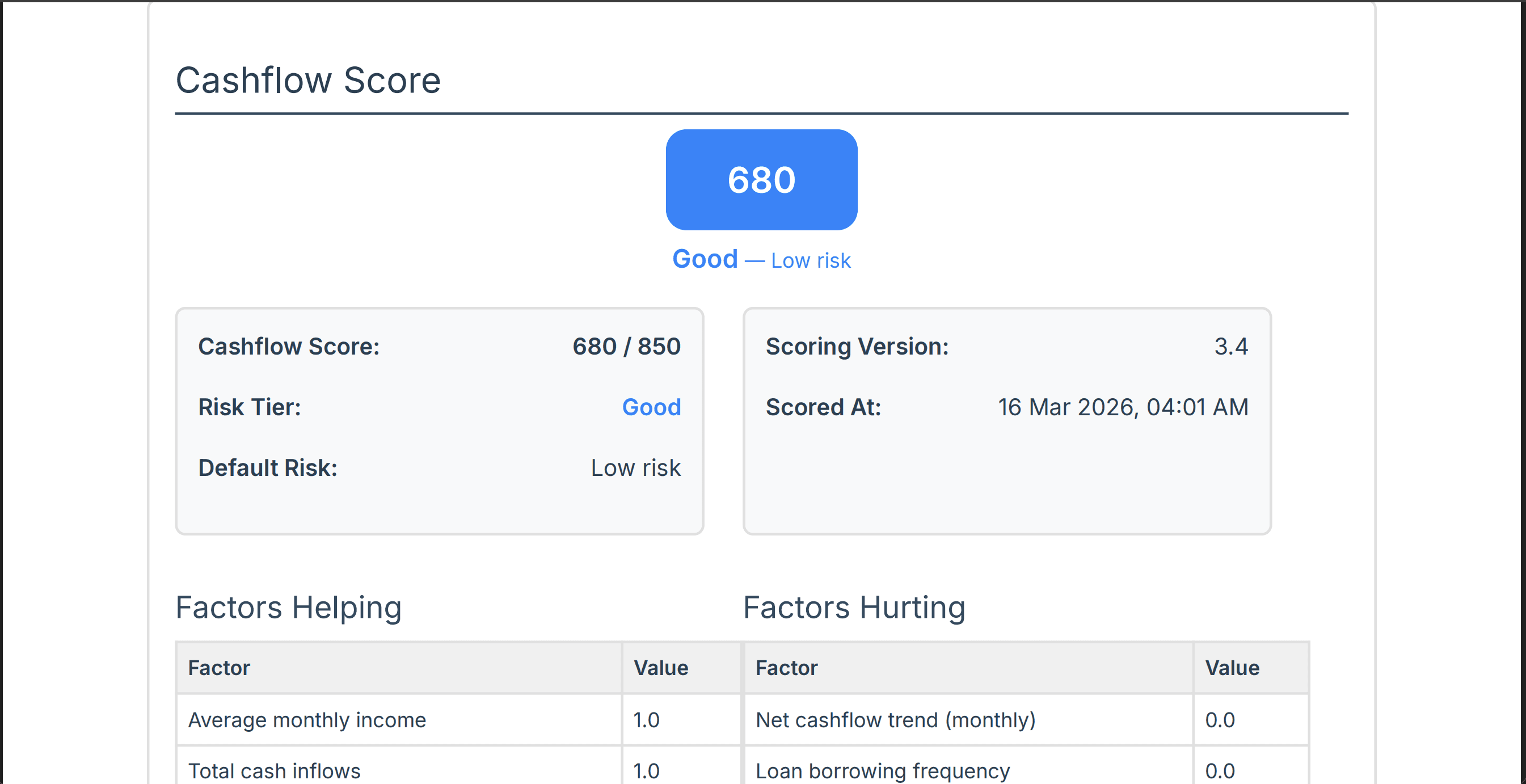

A lender's guide to an AI-powered default prediction score.

Using an Annualized Interest Rate - a 25% for 6 Weeks example If you’re a lender offering short-term loans, you’ve probably dealt with Flat Interest Loans that run for just a few weeks.Let’s say you want to create a loan product that charges a 25% fl...

No black-boxes, no unnecessary complexity—just clear, data-backed decision-making.

Simple, intuitive signals can drive smarter credit decisions

A repayment score measures a borrower's creditworthiness based on their history of repaying loans. It is calculated using information from a borrower's credit report, such as their payment history, amount of debt, and length of credit history.

Repayment scores are typically used by lenders to make decisions about whether to approve a loan and what interest rate to charge.

Repeat clients are borrowers who have previously borrowed money from a lender and have repaid their loans in full and on time. These borrowers are considered to be lower-risk borrowers, and lenders may be willing to offer them more favorable terms on future loans, such as a lower interest rate or a longer repayment term.

One way to reward repeat clients and encourage them to continue borrowing from a lender is to offer them a higher repayment score. This would give them access to more favorable loan terms, such as a lower interest rate or a longer repayment term.

To calculate a repayment score for repeat clients:

Give more weight to recent payments. Borrowers who have made recent payments on time are less likely to default on a new loan, so their repayment score should be higher.

Consider the number of loans repaid. Borrowers who have repaid multiple loans from the same lender are less likely to default on a new loan, so their repayment score should be higher.

Factor in the size of the loans repaid. Borrowers who have repaid larger loans from the same lender are less likely to default on a new loan, so their repayment score should be higher.

Give credit for early repayment. Borrowers who have repaid their loans early are less likely to default on a new loan, so their repayment score should be higher.

By offering repeat clients a higher repayment score, lenders can encourage them to continue borrowing from the lender and reduce the risk of default.

Some of the major parameters that go into the calculations of a repayment score are:

Repayment Start-Date

Repayment End-Date

Expected repayment Day

Expected repayment Amount on each repayment Day

Time intervals in the repayments of an active or an overdue loan

Below is a practical look into the Time Intervals (Streaks)

1. paidStreak

This number represents the longest continuous streak of on-time (fully paid) payments. E.g. if on-time payments were made 5 months in a row, this number will be 5.

2. overDueStreak

This number represents the longest continuous overdue number of payments. E.g. if payments were overdue for 2 months in a row, this number will be 2.

Example

Here is an example of how these variables can be used to assess a borrower's creditworthiness:

Borrower A: paidStreak = 12 overDueStreak = 0

Borrower B: paidStreak = 6 overDueStreak = 1Based on this information, we can conclude that Borrower A has a better credit score than Borrower B. Borrower A has a longer streak of on-time payments and no overdue payments, while Borrower B has a shorter streak of on-time payments and one overdue payment.

The paidStreak and overDueStreak fields can be useful metrics for borrowers to track their creditworthiness and identify areas where they can improve. For example, a borrower with a short paid streak may want to focus on making all of their payments on time and in full.

It is important to note that the paidStreak and overDueStreak fields are just two of many factors lenders consider when making lending decisions. Other factors include;

Credit score: A credit score is a three-digit number that represents a person's creditworthiness. It is calculated using information from a person's credit report, such as their payment history, amount of debt, and length of credit history. A higher credit score indicates a lower risk of default, and lenders are more likely to approve loans for borrowers with high credit scores.

Debt-to-income ratio (DTI): The DTI ratio is a measure of how much debt a person has relative to their income. It is calculated by dividing the total monthly debt payments by the total monthly income. A lower DTI ratio indicates that a person has more disposable income to make loan payments, and lenders are more likely to approve loans for borrowers with low DTI ratios.

Employment history: Lenders also want to see that a borrower has a stable job and income. They will typically look at the borrower's employment history for the past two to three years. A borrower with a long and stable employment history is considered to be a lower risk, and lenders are more likely to approve loans for these borrowers.

Purpose of the loan

Type of loan

Collateral

Down payment

Lenders will use all of this information to assess a borrower's risk and determine whether to approve the loan.

It is important to note that the weight that lenders give to each factor can vary depending on the lender.

Borrowers can improve their chances of getting approved for a loan by improving their credit score, reducing their DTI ratio, and having a stable cashflow.