A Sample Loan Ability Calculator!

Search for a command to run...

No comments yet. Be the first to comment.

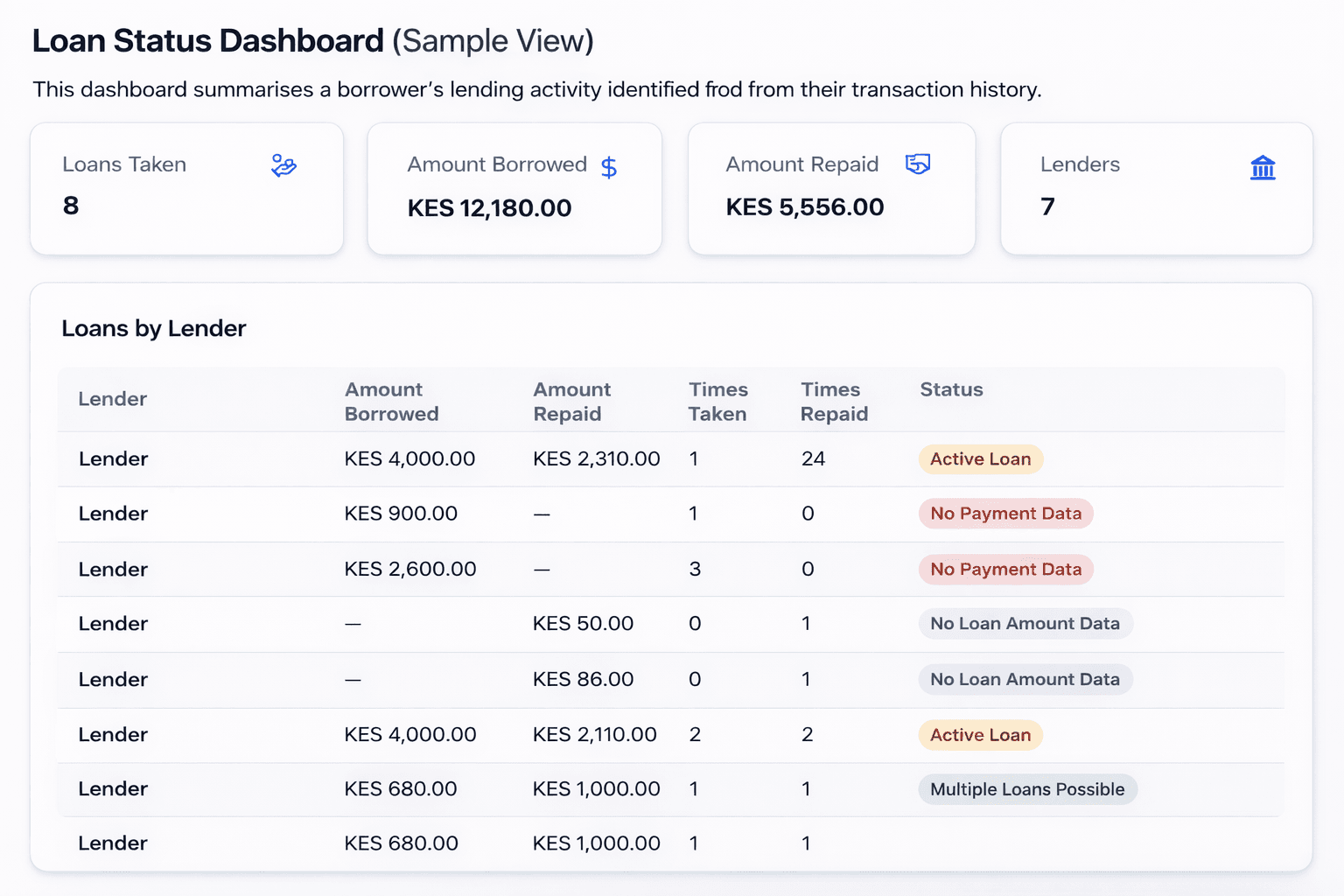

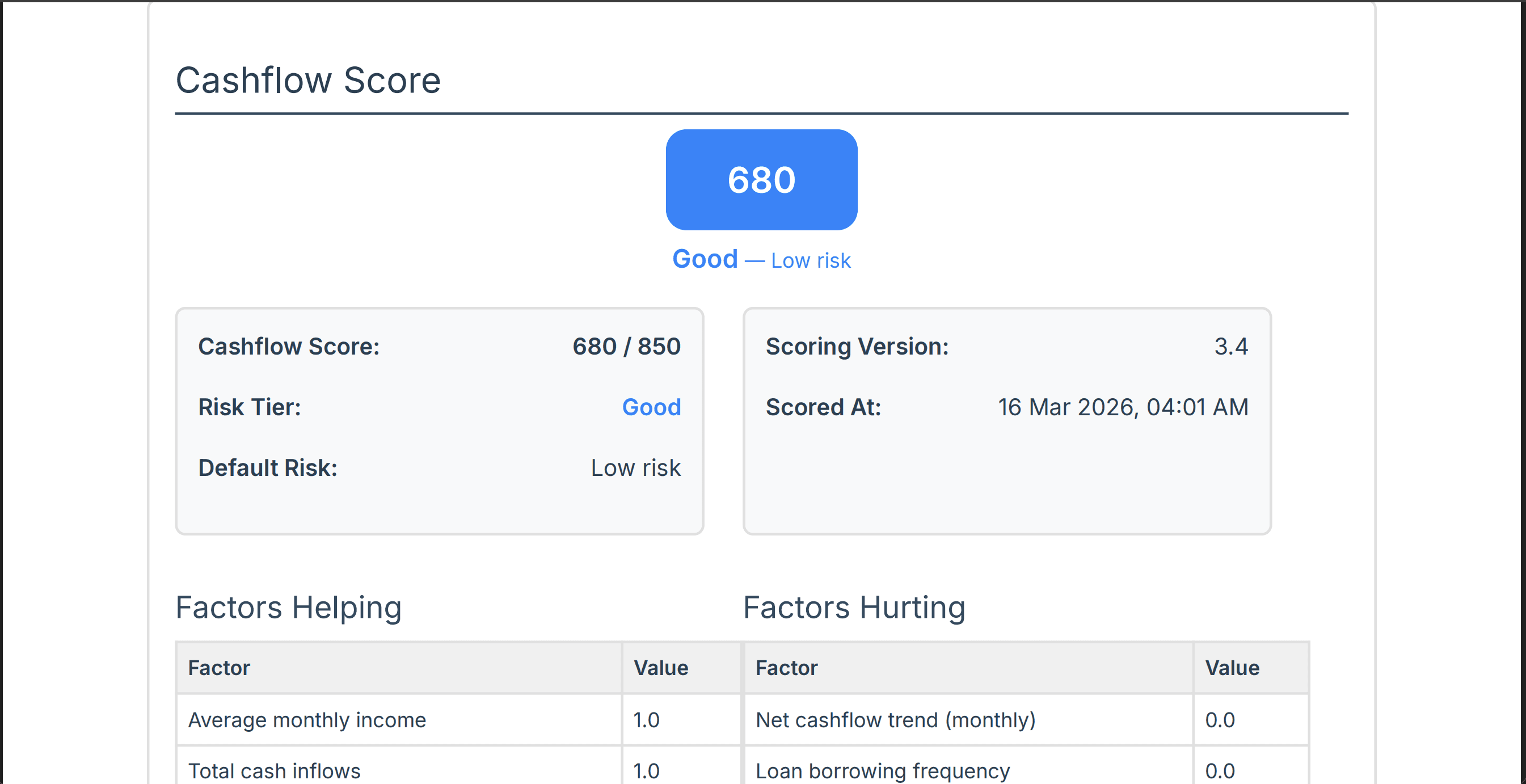

A lender's guide to interpreting loan statuses and cashflow scores in Cladfy reports.

A lender's guide to an AI-powered default prediction score.

Using an Annualized Interest Rate - a 25% for 6 Weeks example If you’re a lender offering short-term loans, you’ve probably dealt with Flat Interest Loans that run for just a few weeks.Let’s say you want to create a loan product that charges a 25% fl...

No black-boxes, no unnecessary complexity—just clear, data-backed decision-making.

Simple, intuitive signals can drive smarter credit decisions

An ability calculator is a tool to help estimate the amount of loan to be approved.

The calculator does not take into account an applicant’s credit score or other factors that may affect the ability to get the loan.

The calculator is based on the provided information and the results may be inaccurate if make were made mistakes during input.

The client is expected to provide supporting documents that illustrate:

Annual income: Ksh

Monthly debt payments: Ksh

Other monthly expenses: Ksh

Outlier transactions: Ksh

The lender will use certain pre-set parameters to compute the estimated loan amount.

Down payment amount: Ksh

Loan term: years

Interest rate: %

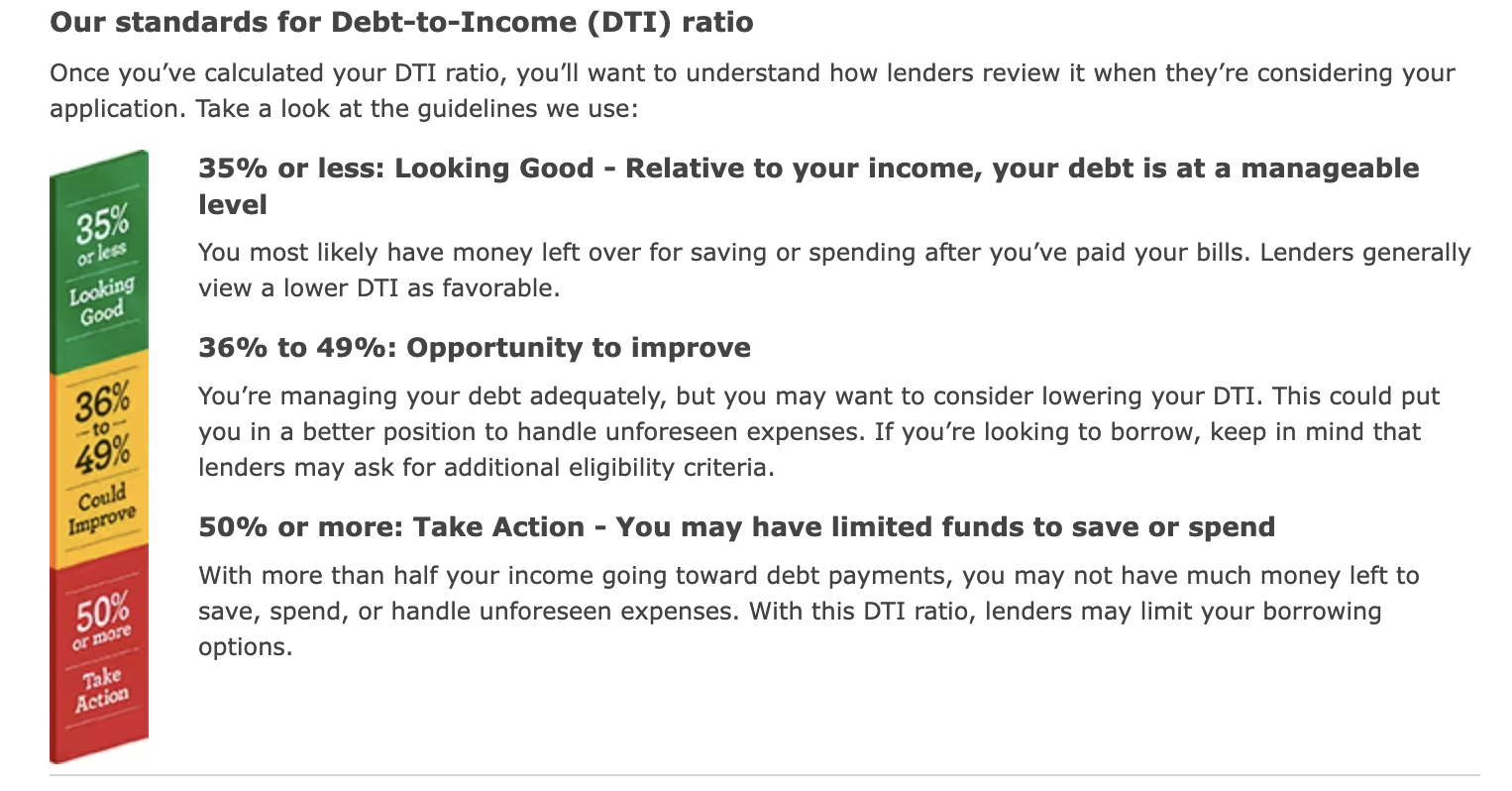

Debt-to-income ratio, DTI: %

Here is a brief explanation of each input field:

Annual income: This is an applicant's total gross income from all sources.

Monthly debt payments: This is the total amount an applicant owes on all of the monthly debts, such as credit cards, car loans, and student loans.

Other monthly expenses: This is the total amount an applicant spends on all of the other monthly expenses, such as housing, food, transportation, and entertainment.

Down payment amount: This is the amount of money an applicant plans to put down on the loan.

Outlier transactions: A financial transaction that is significantly different from the other transactions in a dataset or statement

Debt to Income ratio DTI: % The percentage of an applicant's monthly income that goes towards debt payments. Lenders use DTI to assess the borrower's ability to repay a loan.

Debt-to-income ratio = (Total monthly debt payments) / (Monthly gross income)

An applicant has a monthly gross income of 70,000 Ksh and monthly debt payments of 1000 Ksh

A lender offers a loan with an interest rate of 0f 18%pa and a repayment period of 3 months.

To calculate DTI: Divide the monthly debt payments by the gross monthly income.

DTI = (Monthly debt payments) / (Gross monthly income) = 1000 Ksh / 70,000 Ksh = 1.43%

To Calculate your monthly loan payment. This is the amount of money the borrowers will need to pay back each month on a loan.

Monthly loan payment = (Loan amount) * (Interest rate) / (1 - (1 + Interest rate)^(-Loan period))

Now say the applicant wants to borrow 100,000 Ksh at an interest rate of 18 %pa for a loan period of 3 months, their monthly loan payment would be 3,333.33 Ksh. Calculated as below

Monthly loan payment = (100,000 Ksh) * (0.18) / (1 - (1 + 0.18)^(-3)) = 3,333.33 Ksh

It is important to note that the loan estimate here is suggested and that the actual loan ability may vary depending on individual circumstances that affect both the lender and the applicant.